Losing customers at the point of entry is one of the greatest challenges that banks and financial services providers face, considering the large budgets many have allocated for their digital transformation platforms and major customer experience initiatives on the back of heightened consumer expectations in the last 12-24 months.

As consumers and businesses flock online, the customer onboarding process can make or break a relationship at this crucial point of engagement.

Data from the Experian Global Decisioning Report shows that less than a third of consumers in Asia-Pacific are willing to wait up to 30 seconds before abandoning a variety of online transactions, especially when it comes to accessing their bank accounts online.

The main factors leading to this failed experience are often due to lengthy processes and too much information required from the customer. This culminates in lost revenue even before the customer has had a chance to transact or even experience any products or services.

Best-in-class onboarding experience for banks

Source: Experian, 2021

Source: Experian, 2021

Banks and financial services providers can look to standardise and simplify the digital onboarding journey for greater convenience. But they should also be aware of opportunities to differentiate customers and personalise the experience for all stages of the customer journey, be it online or physical.

Customers at a physical branch are defined in the way they enter, engage, and transact in a branch, while staff can assist and support customers at every step. Online, the process needs to be largely self-service, which requires the platform and experience to be fully automated, intuitive, but also personalised and contextual to be able to adapt to all kinds of customer scenarios.

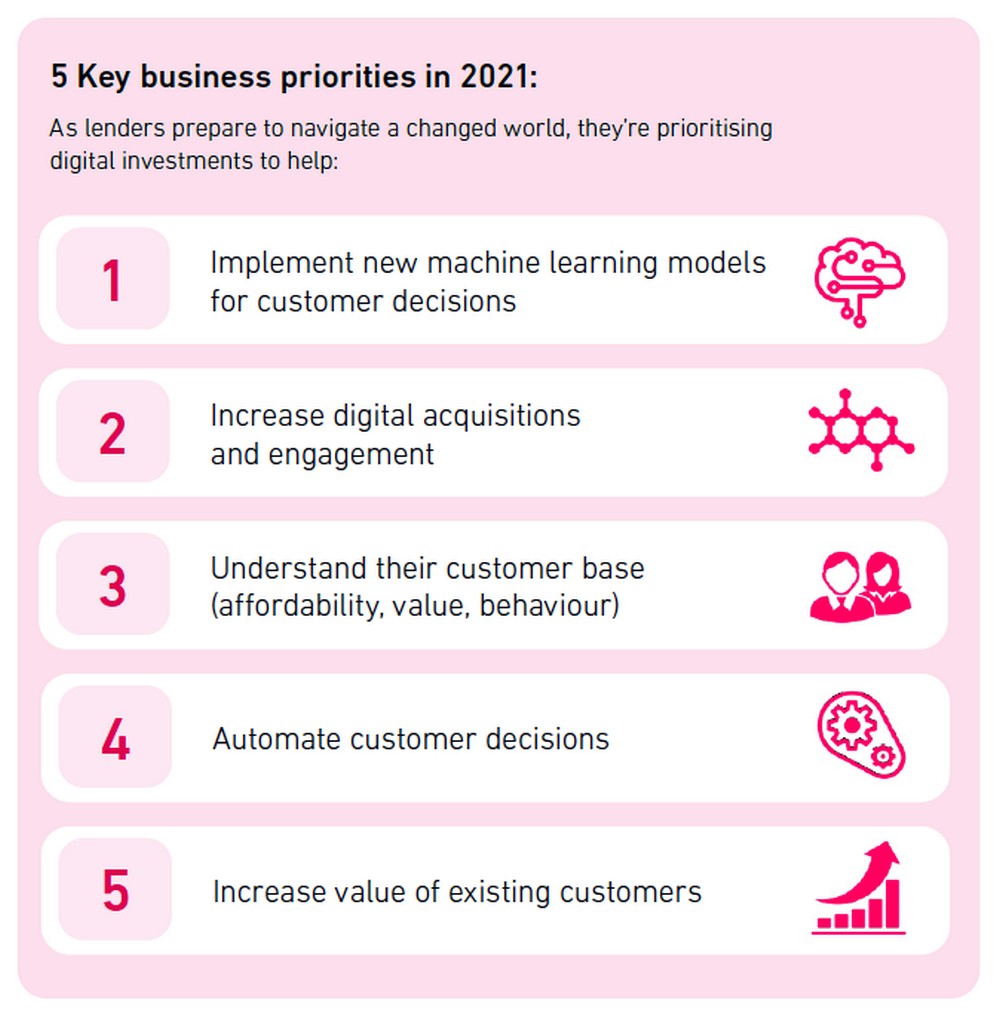

Banks put all their digital transformation efforts at risk without a seamless digital onboarding process in place. In considering the array of technologies available and when building out customer onboarding platforms, there needs to be several key features included, as demanded by customers and important for businesses to succeed in today’s context:

-

- A customer-centric experience – by improving access to services round-the-clock and through a variety of channels to suit target customers.

- Deliver instant approvals – by automating manual processes and returning decisions to customers quicker.

- Reduce customer input, tailor, and minimise information requests according to exact service offering and process

- Reduce customer acquisition costs – through automated decisions to lower labour-intensive manual reviews.

- Make decisions based on rich insight – by combining data to offer the right services to the right customers.

Platform considerations: cloud flexibility is key

A seamless experience that is also successful typically requires significant investment and resources to build and operate sophisticated software systems.

These systems need to dynamically capture a growing amount of data, evaluate risks, perform credit checks, and perform customer acquisition decisions, all while ensuring compliance with regulatory requirements at every stage of the journey in real-time.

As more organisations shift to a hybrid work mode, cloud-based platforms provide flexibility, which is crucial to the success of a hybrid work mode. Furthermore, these platforms can deliver the capabilities of complex in-house systems with lower upfront costs, reduced risk, and constant access to innovative new features.

Experian’s data shows that 80% of organisations intend to integrate on-demand cloud-based decisioning solutions as part of their business strategy in 2021.

Wherever possible, having a pre-configured cloud implementation eliminates months of planning and customisation efforts. A cloud implementation provides multiple benefits when it comes to security and compliance needs.

More importantly, gaining access to automatic updates and a stream of continuous innovation cuts down the time-consuming drain on resources, often due to having to build new features or implementing updates.

Combining customer data at the point of application

Source: Experian, 2021

Source: Experian, 2021

Aside from the business case for cloud-based acquisition platforms, the dependence on data is the most critical element of building a modern seamless onboarding and acquisition capability.

The ability to rapidly connect and draw from multiple data sources, process data, and perform multiple decisions based on an endless permutation of use cases and scenarios should form the core of any enterprise customer acquisition system – with a cloud-based one significantly upping the game.

A successful customer acquisition platform combines customer data at the point of application, with consumer and commercial credit, fraud, and internal data giving banks a comprehensive view to make informed decisions quickly.

The speed of these decisions not only helps identify customers suited to specific products but also improves the overall customer experience by offering round-the-clock decisions to customers who demand intuitive and immediate support. Other key elements that banks need to build into the platform for a successful customer acquisition strategy include:

- Seamless APIs that instantly combine credit, fraud and internal data for acquisition decisions.

- Dynamic reporting dashboard that reviews how processes are performing to help spot any areas for improvement.

- Access to real-time data repository for consumer and commercial credit, ID and fraud to enhance the view of each customer.

- A platform that gives control to broaden and expand the quality of the customer base by creating your own automated acceptance rules.

Adopting strategic digital transformation across the whole customer-facing operation is a journey that promises all the above, but a seamless onboarding and acquisition capability is the first and vital step to maximising your investment and capturing customer opportunities.